All Categories

Featured

Table of Contents

Insurance provider will not pay a minor. Rather, think about leaving the cash to an estate or count on. For even more in-depth information on life insurance policy get a copy of the NAIC Life Insurance Policy Customers Overview.

The IRS positions a limit on just how much cash can go right into life insurance policy premiums for the policy and how promptly such costs can be paid in order for the policy to preserve every one of its tax obligation advantages. If specific limitations are surpassed, a MEC results. MEC insurance holders may be subject to tax obligations on circulations on an income-first basis, that is, to the level there is gain in their plans, along with fines on any kind of taxed quantity if they are not age 59 1/2 or older.

Please note that exceptional fundings build up passion. Income tax-free therapy additionally assumes the loan will become satisfied from income tax-free fatality advantage profits. Finances and withdrawals minimize the policy's cash money worth and death benefit, might trigger specific plan benefits or riders to become unavailable and may increase the chance the plan may lapse.

A customer may certify for the life insurance policy, but not the motorcyclist. A variable universal life insurance contract is an agreement with the main objective of offering a death benefit.

How do I choose the right Cash Value Plans?

These profiles are carefully handled in order to please stated financial investment goals. There are fees and costs related to variable life insurance coverage contracts, consisting of mortality and danger charges, a front-end lots, administrative fees, financial investment monitoring fees, abandonment fees and fees for optional motorcyclists. Equitable Financial and its affiliates do not offer lawful or tax recommendations.

And that's terrific, because that's specifically what the fatality benefit is for.

What are the benefits of entire life insurance? Here are several of the vital points you ought to know. One of the most enticing advantages of acquiring an entire life insurance policy plan is this: As long as you pay your costs, your death advantage will certainly never ever expire. It is assured to be paid no matter of when you die, whether that's tomorrow, in five years, 80 years or even better away. Flexible premiums.

Believe you don't require life insurance policy if you do not have children? There are several advantages to having life insurance, even if you're not sustaining a household.

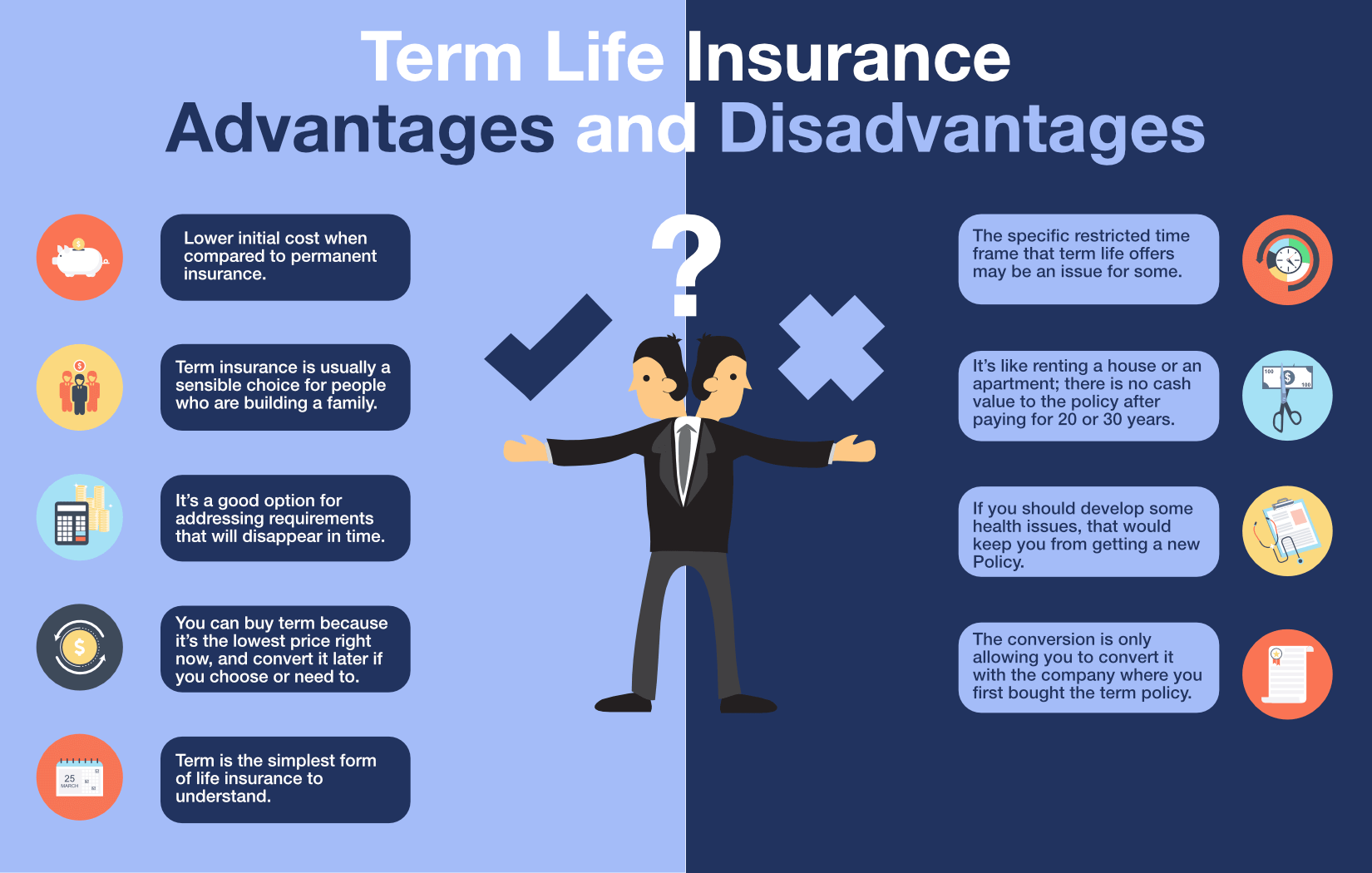

What types of Term Life are available?

Funeral costs, interment expenses and medical bills can include up. Long-term life insurance coverage is offered in various amounts, so you can select a death advantage that meets your needs.

Figure out whether term or permanent life insurance is right for you. After that, obtain a quote of just how much coverage you may require, and how much it might set you back. Discover the correct amount for your budget and comfort. Locate your quantity. As your individual circumstances modification (i.e., marriage, birth of a child or job promo), so will your life insurance coverage needs.

Essentially, there are two kinds of life insurance policy plans - either term or permanent plans or some mix of both. Life insurers use different forms of term strategies and conventional life policies in addition to "rate of interest sensitive" items which have actually become extra common considering that the 1980's.

Term insurance supplies defense for a specified period of time. This duration could be as brief as one year or give insurance coverage for a certain number of years such as 5, 10, twenty years or to a specified age such as 80 or sometimes as much as the oldest age in the life insurance mortality.

What types of Estate Planning are available?

Currently term insurance coverage rates are extremely competitive and amongst the least expensive traditionally experienced. It must be kept in mind that it is a commonly held idea that term insurance is the least pricey pure life insurance policy protection readily available. One requires to evaluate the plan terms thoroughly to decide which term life options are suitable to meet your particular circumstances.

With each new term the costs is enhanced. The right to restore the plan without evidence of insurability is a vital benefit to you. Otherwise, the danger you take is that your health may degrade and you might be not able to obtain a policy at the same rates and even whatsoever, leaving you and your beneficiaries without coverage.

The size of the conversion period will vary depending on the type of term policy purchased. The premium rate you pay on conversion is typically based on your "present acquired age", which is your age on the conversion date.

Under a level term policy the face quantity of the policy stays the same for the entire period. With reducing term the face quantity minimizes over the period. The premium remains the exact same every year. Often such plans are offered as mortgage protection with the quantity of insurance coverage reducing as the equilibrium of the home loan lowers.

What is the process for getting Life Insurance Plans?

Generally, insurance companies have actually not had the right to change costs after the policy is marketed. Since such policies may continue for years, insurance providers have to make use of conservative mortality, rate of interest and expense rate price quotes in the premium computation. Adjustable premium insurance, nevertheless, allows insurance providers to offer insurance at reduced "current" premiums based upon much less conventional assumptions with the right to change these costs in the future.

While term insurance policy is made to offer protection for a defined period, long-term insurance coverage is created to supply coverage for your entire lifetime. To keep the premium price level, the costs at the younger ages goes beyond the real expense of protection. This added costs builds a book (cash money value) which assists spend for the plan in later years as the price of security increases over the costs.

Under some plans, premiums are required to be paid for a set variety of years. Under various other plans, premiums are paid throughout the insurance policy holder's life time. The insurance business invests the excess premium bucks This kind of plan, which is in some cases called money worth life insurance, generates a savings aspect. Cash values are vital to a permanent life insurance policy plan.

{kind=link}

Table of Contents

Latest Posts

Funeral Expenses Benefit

Senior Final Expense

Best Rated Burial Insurance

More

Latest Posts

Funeral Expenses Benefit

Senior Final Expense

Best Rated Burial Insurance